A Significant Cost Avoidance & Consumer Experience Opportunity

Between the 1960s and the 1980s, airlines built a handful of central air booking systems (Global Distribution Systems – like Amadeus and Sabre) to simplify agent access to air fares. Airlines later rebelled against high fees and broke away with direct channels like New Distribution Capabilities (NDC) where premium content skips GDSs entirely. From the 1990s, alternatives of the GDSs in the form of air content aggregators appeared in the market.

At the same time, Corporations when purchasing air travel services, primarily relied on Travel Management Companies via the latter’s GDS solutions. This has been leaving corporations stuck with the dilemma of relying on “incomplete” GDS content at additional costs or opting for cheaper and more comprehensive but equally more complex content management solutions.

Today, because of the solidification of the legacy model many corporate travel programs suffer – rogue bookers bypass designated tools for better deals and services only available on air carriers’ own websites and apps.

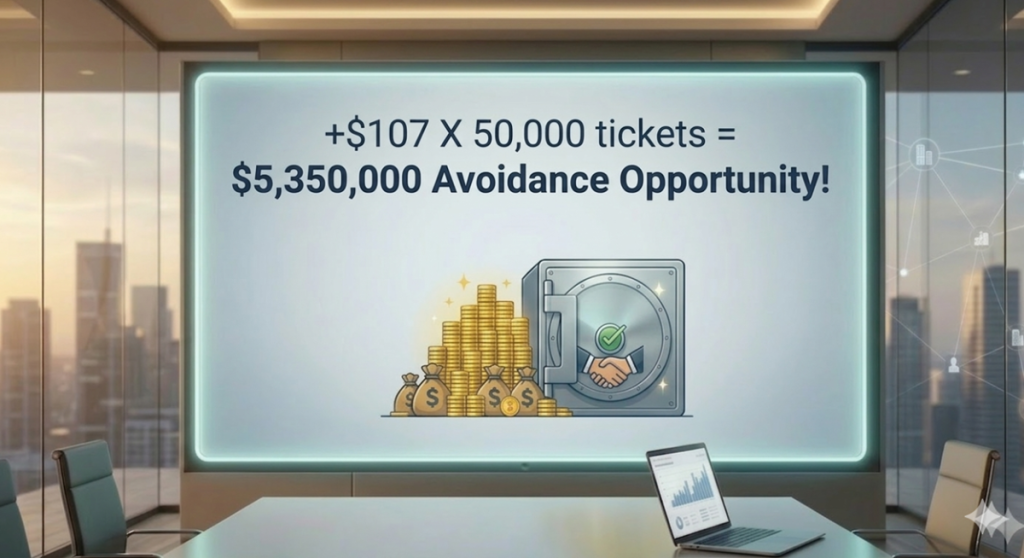

According to Kai-Gordon Weiland, Chief Sales Officer of Atriis – “based on 2025 data (EU/US originating air travel) on average there is a cost difference of over $107 per ticket between NDC and legacy GDS channels”. So, for a medium/large spend corporation which has over 50,000 air tickets annually, we speak about an overspend of $5,350,000 per year, which can amount to a single/double digit percentage of the annual global air spend.

based on 2025 data (EU/US originating air travel) on average there is a cost difference of over $107 per ticket between NDC and legacy GDS channels

Kai-Gordon Weiland, Chief Sales Officer of Atriis

The extent of the issue was confirmed in last year’s BTN State of the Industry reports, the fragmentation of content was highlighted as the first overarching theme of the current state (State-of-the-Industry/2025 – with over 300 respondents primarily from Enterpise/Global Segment Companies).

According to the BTN Survey, Travel Buyers simply cannot get a grip on the problem. Many of them explored way to shift their supplier strategies and steer away from carriers in traditional distribution channels, many did not react at all with suppliers shifts.

Another strategy was to influence the adherence to approved booking channels through strengthening their travel policies, however most companies preferred not to make any changes with their respective policies.

Again, another potential direction was to address the issues with the TMC and OBT partners. Surprisingly, most than two thirds of the respondent did not address it with their respective TMC or OBT partners and only a handful went out to RFP or introduced alternative ways to cope with the problems.

The most recent ITM survey (BTN / ITM Survey) echoed what buyers said in 2025 – the access to content problem was alongside OBT optimization their #1 concern.

At the same time, we also noted that in a very recent article on BTN (BTN-TMC-Content-Opacity) many advocated for the importance of governance, namely, increase the clarity needed around who owns the OBT configurations and policy interpretations. Many argued, that even if the optimal content is available, the correct application of the Clients’ own rules, policies and exceptions need to be correctly translated into the OBT settings and clear policy instructions for agent-assisted bookings.

So why does all this matter and what is at stake? As a result of fragmented content, companies –

- Do not benefit from all available products and services,

- Incrementally pay for services, as they do not benefit from the best available price points and conditions.

Both the first and second consequence leads consumers to go to booking directly with suppliers.

In this context, so what are the right mitigation strategies to address the content fragmentation problems? We would suggest taking the following steps –

- Request your air carrier representative to provide channel adoption (channel breakdown) reports on what was booked via NDC-enabled and what was booked via EDIFACT (GDS) channels. These should also include metrics of savings to benefitting from Continuous Pricing/Exclusive Content, the utilization of corporate bundles/ancillaries and the savings due to avoiding GDS surcharges,

- Audit simultaneously your own designated channels vs 3rd party, consumer channels to assess access to the major spend air carrier fares. Observe gaps in fare and content parity, ancillaries,

- Interview your TMC and OBT suppliers and ask for specific metrics around NDC enablement for large spend air carriers,

- Check the OBT settings and make sure NDC content is enabled,

- Audit GDS surcharges on large spend air carriers,

- Look into corporate fare usage/adoption where applicable,

- Dig into off-channel bookings by looking at reason codes.

- Assess how NDC solutions in place are working – do they provide the operational consistency, the servicing depth and the reliability needed?

- Depending on the availability of NDC solutions – address options with GDS and non-GDS content providers. This also eases the discussion with the TMC&OBT parties, as the discussion with the former (GDS/non-GDS content providers) creates more transparency around market capabilities.

Once the outcomes of this larger audit effort and discussions are available, you need to set the ambitions for the future. The TMC, OBT, GDS and non-GDS content partners are crucial to work with hands-in-hands, and their firm commitment to elevate their game is a must.

Also, the above raises questions about what the right governance is when it comes to who owns the policy settings, the OBT configurations. Checks and balances need to be introduced to keep all supplier parties motivated to optimise content for their customer.

If the above have inspired you and you would like to discuss further the above, please get in contact with us.